The Money Fight Every Marriage Has, and How to Actually Win It

You and your husband have had the same fight about money four different ways this year. Sometimes it is about a credit card statement. Sometimes it is about who forgot to pay the electric bill. It never actually feels like it is about the number on the screen. For women aged 25 to 50 navigating this exact pattern in 2026, money fights in marriage rarely stay contained to money. They pick up old resentments about fairness, control, and who gets to feel secure.

I am Maya Collins, and while my own money story runs through single parenting and rebuilding from almost nothing, I hear from married readers constantly asking some version of the same question. How do you stop the fighting when you both work hard and it still feels unfair? The answer is not “communicate more.” That advice is true and also useless without a system underneath it.

This guide walks through what actually works when money fights in marriage have become a pattern instead of a rare bad night.

To stop money fights in marriage, couples need three things working together: full transparency about debts and income, a shared account structure that both partners helped design, and a recurring short meeting to review the numbers before small issues become big ones. Most fights are not about the dollar amount. They are about one partner feeling unseen or unfairly burdened, and a system fixes that faster than a conversation alone ever will.

Why “Just Talk About Money More” Doesn’t Fix Anything

Every marriage advice column says the same thing. Communicate. Be open. Talk about money early and often. None of that is wrong, but it treats communication like a switch you flip rather than a skill you build.

If you and your husband already avoid the topic, telling yourselves to “just talk more” is like telling someone with a bad knee to just run more. You need the underlying structure first: a defined space to talk (a real meeting, not a fight that erupts over dinner), a shared vocabulary for what you are each afraid of, and a system that makes the conversation about decisions instead of blame.

Financial secrecy, sometimes called financial infidelity, is hiding purchases, accounts, or debts from a spouse. It erodes trust the same way any other kind of secrecy does, and it is one of the fastest ways a small money disagreement becomes a marriage-threatening one. Naming it clearly, even if neither of you has done anything that dramatic, gives you both language for why full disclosure matters.

The Actual System That Stops the Fighting

Here is what a working system actually looks like, step by step.

Start with full disclosure. Before any account structure or budget can work, both partners need to see the complete picture: student loans, credit card balances, any hidden accounts, and current income. This is uncomfortable exactly once. Couples who skip this step end up building a budget on incomplete information, which guarantees it collapses the first time a surprise bill shows up.

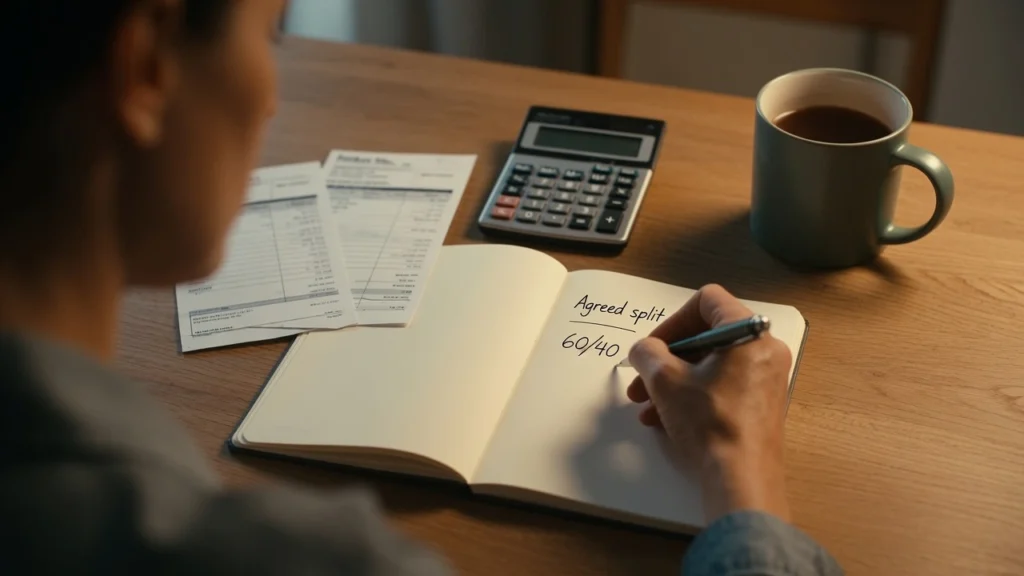

Pick an account structure you both actually chose. There are three common models. In the fully joint model, all income goes into one account and every expense comes from it. In the joint-plus-allowance model, both incomes go into a shared account for bills, mortgage, and savings, and each partner keeps a small personal allowance to spend without explaining it. In the proportional model, each partner contributes to shared expenses based on a fixed ratio of income rather than splitting everything 50/50.

If you earn $80,000 and your husband earns $50,000, a straight 50/50 split on a $2,000 monthly expense pile means you are contributing a smaller share of your income than he is. A proportional split based on that same $80,000 and $50,000 income ratio has you covering roughly 62 percent of shared costs and him covering roughly 38 percent, which keeps the burden proportionate rather than technically equal.

Automate what you can. Automatic payments on recurring bills remove one entire category of fight: the “I thought you paid that” argument. This single change eliminates a surprising number of arguments that were never really about money at all, they were about a missed task.

How to Split Money When One Partner Earns More

This is worth its own space because it is the single most common source of resentment in the brain dump behind this guide, and in reader messages I get. The proportional model above solves the math. What it does not automatically solve is the emotional side, where the lower earner sometimes feels like a junior partner even when the ratio is fair on paper. Naming that feeling out loud, in a calm meeting rather than mid-argument, matters as much as the spreadsheet does.

Money Fights in Marriage: What the Numbers Actually Look Like

Money fights in marriage tend to follow a predictable arc when there is no system in place: a bill or a purchase triggers it, the argument escalates into old grievances, nothing gets resolved, and the same fight resurfaces within weeks. Building the system above interrupts that arc at the trigger point instead of after the escalation.

I am not a financial advisor and this is not financial advice. For your specific situation, especially around debt, joint accounts, or major financial decisions, talk to a qualified professional.

What the Research Actually Says About Money and Marriage

According to the Federal Reserve’s Report on the Economic Well-Being of U.S. Households, a meaningful share of American households report they could not comfortably cover an unexpected expense without borrowing or cutting back elsewhere. That single fact explains a lot about why money fights in marriage escalate so fast. When there is no cushion, every unplanned expense becomes a crisis instead of an inconvenience, and crises make people defensive.

According to the Consumer Financial Protection Bureau, transparency around existing debt, including student loans and credit card balances, is one of the most consistently cited factors in whether couples successfully manage shared finances without ongoing conflict. That lines up with the disclosure step above: it is not optional, it is foundational.

An emergency fund, money set aside specifically for unplanned expenses like a job loss or car repair, changes this dynamic directly. Couples with even a partial cushion have more room to solve a surprise expense together instead of fighting about whose fault it is.

What Changes Once You Have a System

Couples who put a real structure in place do not stop disagreeing about money entirely. What changes is the shape of the disagreement. Instead of “you never think about the future,” the conversation becomes “should we adjust our proportional split now that your income changed.” Instead of blindsiding each other with purchases, you are working from numbers you both already agreed to.

The fights that remain tend to be smaller and shorter, because most of the fuel, secrecy, unfairness, and surprise, has already been removed from the situation. That is a realistic goal. Zero disagreements is not.

People Also Ask

How do couples split finances when one person makes more money?

Most couples use either a straight 50/50 split, a joint account with personal allowances, or a proportional split based on each partner’s income ratio. Money fights in marriage often ease up when couples switch from an equal split to a proportional one, since it removes the sense that the lower earner is contributing an unfair share relative to their income.

What is financial infidelity in a marriage?

Financial infidelity is hiding purchases, debts, or accounts from a spouse. It functions like any other form of secrecy in a relationship and is one of the fastest paths from an ordinary disagreement to a serious trust problem. Full disclosure of debts and income is the first step in stopping this pattern before it starts.

Should married couples have joint bank accounts or separate ones?

Neither structure is inherently right or wrong, but separate accounts should never be used to hide financial activity from a spouse. Many couples reduce money fights in marriage by using a joint account for shared bills alongside small personal allowances each partner can spend without oversight or explanation.

How often should married couples talk about money?

A short, regular meeting, weekly or monthly depending on the couple, works better than sporadic conversations that only happen after a fight. Treating it as a scheduled check-in rather than a crisis conversation is one of the most effective ways to reduce money fights in marriage over time.

The One Conversation to Have This Week

You do not need to fix your entire financial life this weekend. You need one honest conversation and one small structural change.

Pick a specific time this week, not “sometime soon,” and use it for exactly one thing: full disclosure of where you both stand financially right now. No budget, no blame, just the real numbers. From there, decide together which account structure fits your situation, even if it is imperfect at first. If building a real emergency fund feels overwhelming right now, start smaller than feels meaningful. Money fights in marriage lose most of their power the moment both partners can see the same picture.