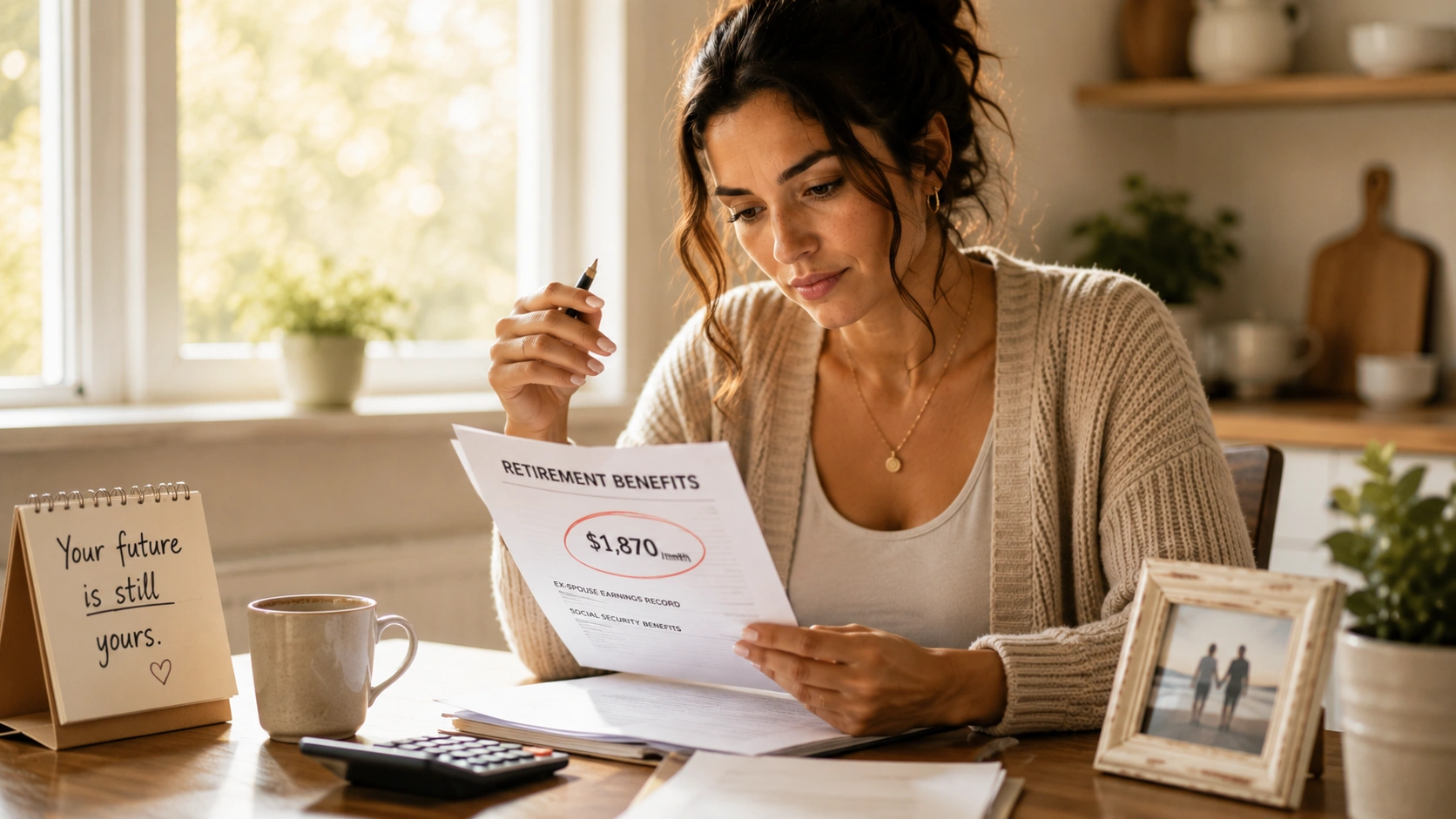

She is sitting at the kitchen table with the divorce paperwork spread out in front of her, the same table where she used to pay bills as half of a couple. Nobody in this process has mentioned what happens to the retirement account she never had her own name on, the one built entirely on her ex-husband’s paychecks over twenty-some years.

That silence is not an accident. Divorce paperwork covers who keeps the house and who keeps the car. It rarely mentions Social Security benefits for divorced and widowed women, or that she may still be entitled to a real, ongoing piece of his record, sometimes worth hundreds of dollars a month for the rest of her life, and that this entitlement has nothing to do with whether he ever finds out, agrees, or remarries.

Widowed women face a version of this same silence from a different direction. A husband’s death brings paperwork too, a funeral to plan, accounts to close, insurance to sort through, and somewhere in that overwhelming pile sits a Social Security decision that most women are never walked through clearly, at exactly the moment they have the least bandwidth to research it themselves.

Divorced spouse benefits let a woman married ten years or longer claim Social Security based on her ex-husband’s earnings record, worth up to 50 percent of his full retirement age benefit, even if he remarried. If he has since died, she may qualify instead for a survivor benefit worth up to 100 percent. Neither requires his permission.

Why Most Retirement Advice Fails Divorced and Widowed Women

Almost every piece of retirement content written for women assumes a fairly linear, uncomplicated life, one marriage, one household income, one shared plan for old age spent together. That assumption quietly erases an enormous number of real situations, a marriage that ended in divorce after fifteen years, a husband who died before either of them reached retirement age, a second marriage after a first one ended badly. When the advice does not account for these situations, women in exactly these situations conclude, reasonably but incorrectly, that the advice simply does not apply to them anymore.

That gap matters more than it might seem, because divorced spouse benefits and survivor benefits are not obscure loopholes. They are standard, well established parts of how Social Security works, built specifically to protect a spouse who spent years out of the paid workforce or earning significantly less than a husband did. A woman who left a marriage with little to her name on paper may still have a real financial asset sitting untouched, one tied entirely to a marriage that has already ended.

Part of the problem is structural. Most retirement content is written to a general audience and optimized to avoid anything that sounds too specific or too legal, which means the genuinely useful, specific rules end up flattened into vague reassurance instead. Real Social Security benefits for divorced and widowed women deserve more than a generic reminder to save for retirement. A woman searching for real answers about her exact situation, a ten year marriage, an ex-husband who remarried, a spouse who died before either of them retired, deserves the actual eligibility rules that apply to her specific circumstances, stated plainly and completely enough to act on with real confidence.

The confusion gets worse after a divorce specifically, because both people involved often assume claiming on an ex-spouse’s record requires his cooperation, his awareness, or his approval. None of that is true. The Social Security Administration does not notify an ex-spouse when a former partner files a claim based on his earnings record, and doing so has zero effect on what he or a current spouse eventually receives. This is one of the most consistently misunderstood pieces of the entire system, and misunderstanding it costs real women real money every single year.

Widowhood carries its own version of the same confusion, layered on top of grief that makes careful research feel impossible. A woman who lost a husband is often focused entirely on the immediate aftermath, and by the time she has the bandwidth to think about long-term finances, months have sometimes passed without anyone mentioning that a survivor benefit exists, that it can be worth significantly more than a divorced spouse benefit would have been, or that claiming it involves its own set of timing decisions that are difficult to undo once made.

Funeral homes, estate attorneys, and even well-meaning family members rarely bring up Social Security in the immediate aftermath of a death, not out of any bad intent, but because it simply is not their area of expertise. The gap between what a grieving widow actually needs to know and what anyone around her thinks to mention is where real, claimable money quietly goes unclaimed for months or, in some cases, years.

How Divorced Spouse Benefits Actually Work

A divorced spouse benefit lets a woman claim Social Security based on an ex-husband’s work record instead of, or in addition to, her own. The core eligibility rule is straightforward. The marriage must have lasted at least ten years, she must currently be unmarried, and she must be at least 62 years old. Her ex-husband must be eligible for his own Social Security retirement or disability benefit, meaning he has worked long enough to qualify, typically at least ten years of covered work himself.

It helps to separate what this benefit is from what it is not. It is not alimony, and it has no connection to any court order from the divorce itself. It exists entirely within Social Security’s own rules, independent of whatever the divorce settlement decided about property, support payments, or anything else. A woman does not need her divorce decree to mention Social Security at all for this benefit to exist and apply to her.

Here is the detail that surprises almost everyone. Her ex-husband does not need to have already filed for his own benefits for her to claim hers, as long as the divorce has been final for at least two years and he is at least 62 himself. This two year rule exists specifically so that a woman is not stuck waiting on an ex-husband’s own timeline or willingness to file before she can access money she is independently entitled to. It is one of the most consequential, least understood rules in this entire system, since it removes the single biggest practical obstacle most women assume stands in their way.

The benefit amount, if she qualifies, is calculated as up to 50 percent of her ex-husband’s full retirement age benefit. Full retirement age, sometimes shortened to FRA, is the specific age set by the Social Security Administration at which a person qualifies for their complete, unreduced benefit, and it varies slightly depending on birth year. This is not 50 percent of whatever he actually receives if he claimed early or late.

Claiming before her own full retirement age reduces this amount permanently, in the same way claiming her own retirement benefit early would. Social Security never pays both a full retirement benefit and a full divorced spouse benefit stacked together. If she qualifies for both based on her own work history and her ex-husband’s, she receives whichever single amount is higher, not the sum of the two.

If You’ve Been Married More Than Once

A woman with more than one marriage that ended in divorce, each lasting ten years or longer, can potentially compare benefits from each former marriage and claim whichever produces the highest payment. Nothing about a second or third marriage cancels out eligibility from an earlier one, as long as each marriage independently meets the ten year threshold. This is one of the more overlooked corners of the rule, since most people assume only the most recent marriage counts toward anything.

Comparing across multiple former marriages does require some legwork, since each one is evaluated on its own ex-spouse’s earnings record. Requesting an official benefit estimate for each scenario directly through the Social Security Administration, rather than guessing based on rough math, is the only way to know for certain which option actually pays the most.

Full retirement age itself is genuinely not the same for every woman. According to Social Security Administration rules, it depends on birth year, generally landing at 66 for those born in the mid-1950s and gradually rising to 67 for anyone born in 1960 or later. Knowing your own specific full retirement age, rather than assuming it is a single fixed number for everyone, is a necessary first step before any of the percentages discussed here can be applied accurately to your situation.

Applying for this benefit involves more paperwork than most women expect, mostly because the Social Security Administration needs to confirm a marriage that, on paper, no longer exists. A final divorce decree is typically required, along with a marriage certificate if one is still available, and your own social security number.

If any records from the marriage are missing after this many years, the Social Security Administration can often help locate them, though the process moves faster when a woman keeps her own copies of these documents rather than relying on an ex-husband to produce his. Starting this document search well before you plan to actually file, even years in advance, is one of the simplest, most concrete things a woman can do today to make the eventual claim far smoother.

The application itself can be started online, over the phone, or in person at a local Social Security office, and an appointment, while not strictly required, tends to shorten how long the whole process takes. Expect to answer detailed questions about the marriage itself, its start and end dates, and whether either party has remarried since, since these details directly determine eligibility. None of this requires anything from the ex-husband directly. The burden of proof sits entirely on the documents a woman herself can gather.

Gathering these documents now, well before actually filing, saves real stress later. A certified copy of the marriage certificate, the final divorce decree, and a record of the ex-husband’s full name, date of birth, and social security number if it is known, are the core pieces worth locating and keeping somewhere safe. Many women do not have easy access to an ex-husband’s social security number years after a divorce, and the Social Security Administration can typically still process a claim using other identifying information, so a missing number should not stop anyone from starting the process out of a mistaken belief that it disqualifies her.

Losing all contact with an ex-husband over the years, sometimes for decades, is common and does not disqualify a woman from this benefit either. The Social Security Administration has its own internal records tied to a person’s social security number and can typically locate a match using the identifying details a woman already has, even without a current address or any recent contact. Not knowing where an ex-husband currently lives, or whether he is even still working, is a reason to start the application process sooner rather than a reason to assume the claim is impossible.

Widow And Survivor Benefits: What Changes When An Ex Has Passed

If a former husband has died, the benefit picture shifts from a divorced spouse benefit to a survivor benefit, sometimes called a surviving divorced spouse benefit when the marriage ended before his death. This version of the benefit can be worth considerably more than the divorced spouse benefit was while he was alive, up to 100 percent of his full benefit rather than 50 percent, depending on the age at which she claims it.

This is one of the areas where Social Security benefits for divorced and widowed women differ most significantly from each other, even though both start from the same underlying marriage, and understanding which one currently applies to your specific situation is the single most important first step before any of the numbers below become meaningful.

The same ten year marriage rule applies here as well. If she was married to him for ten years or more before the divorce, she remains eligible for survivor benefits on his record even though the marriage ended long before his death. Claiming at her own full retirement age typically provides the full survivor amount, while claiming between age 60 and her full retirement age results in a reduced percentage, generally somewhere between 71.5 percent and 99 percent of his full benefit depending on exactly how early she claims.

A widow caring for his child who is under age 16, or a disabled child of any age, may qualify for survivor benefits earlier than 60 under a different set of rules entirely, and in this specific situation the ten year marriage length requirement does not apply the same way, since the benefit is tied to caring for his child rather than to the marriage length itself.

This particular path matters enormously for a younger widow, one in her thirties or forties with children still at home, who might otherwise assume survivor benefits are something reserved for retirement age decades away. A woman in this situation should contact the Social Security Administration as soon as possible after a spouse’s death, since this version of the benefit can begin providing real, ongoing support immediately rather than waiting until age 60 like most other survivor scenarios require.

Disability changes the age math significantly, and it is worth understanding even if it does not apply to your situation today, since circumstances change. A widow or surviving divorced spouse who is disabled can potentially claim survivor benefits as early as age 50, a full decade earlier than the standard threshold, provided the disability meets the Social Security Administration’s own definition and documentation requirements. This is one of the least publicized corners of the entire survivor benefit system, largely because it applies to a smaller group of women, but it matters enormously to the women it does apply to.

There is also a separate, smaller benefit worth knowing about. Social Security pays a one time lump sum death payment of $255 to an eligible surviving spouse or surviving divorced spouse, according to Social Security Administration rules. It is a modest amount, but it is real money that goes unclaimed surprisingly often simply because people do not know to ask for it.

The Remarriage Rule Nobody Explains Well

Remarrying can affect survivor benefit eligibility, but the rule is more forgiving than most women assume. Remarrying before age 60 generally ends eligibility for a survivor benefit based on a prior marriage. Remarrying at age 60 or later does not affect that eligibility at all, and she can still choose to claim survivor benefits from the earlier marriage even while remarried. The exact same age 60 threshold drops to 50 if she is disabled. This single detail has real financial weight for any woman considering remarriage later in life who has a survivor benefit sitting on an earlier marriage’s record.

The practical impact of this rule shows up most clearly for a widow in her late fifties who is dating someone seriously and considering marriage. Waiting until her sixtieth birthday to formalize a new marriage, if a survivor benefit from a prior marriage would otherwise be meaningfully large, is not a romantic compromise so much as a financial decision worth having with full information rather than discovering the rule after the fact. A divorced spouse benefit from a living ex-husband works differently and typically ends upon any remarriage at any age, which is an important distinction from the survivor benefit rule and a common source of confusion between the two.

Nobody should feel pressured to delay a relationship purely over a benefit calculation, and that is not the point being made here. The point is simply that this is a decision worth making with accurate, complete information rather than discovering the financial consequence of timing after the fact, when there is no way to undo an already finalized marriage.

I am not a financial advisor and this is not financial advice. For your specific situation, especially one involving remarriage timing or comparing multiple potential benefits, talk to a qualified professional or contact the Social Security Administration directly before making a decision that is difficult to reverse.

The Hard Numbers Behind These Benefits

According to the Social Security Administration, a divorced spouse benefit can be worth up to 50 percent of an ex-husband’s full retirement age benefit, while a survivor or surviving divorced spouse benefit can be worth up to 100 percent of his full benefit, with the exact percentage depending heavily on the age at which it is claimed. Claiming any of these benefits before full retirement age results in a permanent reduction, the same way claiming an individual’s own retirement benefit early does.

| Benefit Type | Marriage Length Required | Maximum Amount | Earliest Claiming Age |

|---|---|---|---|

| Divorced spouse benefit (ex living) | 10 years or more | Up to 50% of his full benefit | 62 |

| Surviving divorced spouse benefit | 10 years or more | Up to 100% of his full benefit | 60, or 50 if disabled |

| Survivor benefit, caring for his child | No minimum length specified | Based on his full benefit | Any age, if child is under 16 or disabled |

| One time death payment | Applies to eligible spouses and surviving divorced spouses | $255 flat amount | Applied for after death |

The one time death payment mentioned in the table, $255, has stayed at that same fixed amount for a very long time and is paid separately from any ongoing monthly benefit. It requires an application and is not paid automatically, which is exactly why so many eligible widows and surviving divorced spouses never receive it.

Picture a concrete example instead of an abstract percentage. If a woman was married for fourteen years to a man whose full retirement age benefit works out to $2,400 a month, her divorced spouse benefit, claimed at her own full retirement age, could be worth up to $1,200 a month, half of his amount. If he later passes away, that same relationship could shift to a surviving divorced spouse benefit worth up to the full $2,400, again depending on the age at which she claims it.

That difference, $1,200 a month versus potentially double that amount, is exactly why understanding which category currently applies to a specific situation matters so much, and why assuming the smaller, divorced spouse version is the only option available can be a costly assumption if circumstances have since changed.

Exact numbers for any individual situation depend entirely on the ex-spouse’s specific earnings history, which only the Social Security Administration can calculate precisely. A rough estimate found through unofficial calculators online is a starting point for curiosity, not a number to plan a retirement around. Requesting an official benefit statement or estimate directly is the only way to get a number worth actually relying on.

One additional factor worth knowing about, even though it applies to a smaller group of women, is the Government Pension Offset. If a woman receives a pension from government work where she did not pay into Social Security, her survivor or ex-spouse entitlement can be reduced significantly, according to Social Security Administration rules. This most often affects women who spent part of their career in certain public sector jobs, and it is exactly the kind of detail worth confirming directly with the Social Security Administration rather than assuming it does or does not apply to a specific work history.

None of these figures are meant to replace a conversation with the Social Security Administration itself. They exist so that a woman walking into that conversation, whether by phone, online, or in person, already understands roughly what she is asking about and can ask sharper, more specific questions instead of starting from zero, which tends to make the entire process feel far less intimidating than it does before that first conversation happens.

The Mistakes That Cost Women Real Money

These are not rare, unusual errors. They are the same handful of misunderstandings that come up over and over again, year after year, across countless different women’s lives, often because nobody explained the actual rule clearly at the moment it mattered most.

This matters most for a specific group of women who rarely see themselves reflected in mainstream retirement content, women in their fifties and sixties going through a divorce after a long marriage, women who lost a husband before either of them reached traditional retirement age, and women who spent years out of the paid workforce raising children and now genuinely worry their own earnings record alone will not be enough. None of these situations are rare. All of them come with real, specific entitlements that a general retirement article aimed at married couples simply never addresses.

The single most common mistake is never applying at all, because a woman assumes, incorrectly, that she needs her ex-husband’s permission, awareness, or cooperation to file a claim based on his record. She does not need any of the three. Filing does not notify him, does not require his signature, and does not reduce what he receives.

The second common mistake is assuming an ex-husband must have already filed for his own benefits before she can claim hers. As covered earlier in detail, the two year rule removes that requirement entirely for most divorced women, as long as he is old enough to qualify himself.

The third mistake is remarrying before age 60 without realizing it permanently closes the door on a survivor benefit from an earlier marriage that may have been worth considerably more than anything available through a current marriage. This is rarely explained clearly anywhere outside of a Social Security office, and by the time most women learn the rule, the decision has already been made and cannot be undone.

The fourth mistake, and possibly the most expensive one, is never comparing all the benefits a woman may actually be eligible for, her own earned retirement benefit, a divorced spouse benefit, and a survivor benefit from a different marriage entirely if she has more than one in her history. Social Security pays whichever single amount is highest, but it does not automatically calculate every possible comparison for her unless she specifically asks.

The fifth mistake is assuming a rough online calculator’s estimate is close enough to plan around. These tools can be a reasonable starting point for curiosity, but they generally cannot access an ex-husband’s actual earnings record, which means the real number could be meaningfully different in either direction. A decision as significant as when to claim, or whether to delay a new marriage, deserves an actual figure from the Social Security Administration itself, not an estimate built on averages.

None of these five mistakes require any special financial background or professional training to avoid. They require knowing the rules exist in the first place, which is exactly the gap this entire guide is trying to close for a woman who has never had a reason to sit down with a retirement specialist and ask about her own specific situation. Most women who eventually do file describe the actual conversation with the Social Security Administration as far less complicated than they expected, once they arrive with the right documents already gathered and a clear sense of which benefit they are actually asking about.

What Changes Once You Actually Claim

Claiming a benefit she was already entitled to does not feel dramatic in the moment, no ceremony, no announcement, just a deposit that starts arriving on a schedule instead of money that was always hers sitting unclaimed. What actually changes is quieter than that. A woman who spent years worried about retirement income tied entirely to a marriage that no longer exists gets to stop worrying about a piece of it, because that piece was never actually contingent on the marriage continuing in the first place.

It also changes the shape of a retirement conversation that often felt entirely closed off after a divorce or a spouse’s death. Instead of starting retirement planning from zero, a woman claiming one of these benefits is starting from whatever baseline that benefit provides, which for many women is a meaningfully higher number than planning around only her own earnings record would have produced.

For a woman who left a marriage with little in her own name, this shift can carry weight well beyond the monthly deposit itself. It is proof that decades spent raising children, managing a household, or earning less than a husband did were not simply erased when the marriage ended. The system, imperfectly and slowly, accounted for that imbalance. Claiming what she is owed is not asking for a favor. It is collecting an entitlement her own life circumstances already earned.

This also reshapes how a woman talks about money with the people around her. Adult children, siblings, or a new partner often assume a divorce or a spouse’s death simply erased any connection to a former marriage’s finances entirely. Being able to explain, clearly and without apology, that a real entitlement still exists and has already been claimed tends to shift the entire family conversation from worry to something closer to relief, and it often prompts other women in her life, sisters, friends, coworkers going through their own divorces or widowhoods, to ask the same questions about their own situations for the first time.

For a woman who has spent years being told, directly or indirectly, that her financial future depends entirely on decisions someone else made, filing this claim is a small act of taking back something that was already hers under the rules the whole time. It does not undo a difficult marriage or a painful loss. It simply makes sure the years she gave to that marriage are reflected honestly in what she receives now, and that recognition, quiet as it is, tends to matter more over time than the dollar amount alone ever fully captures.

The Honest Summary

Filing for either of these benefits is not instant. Expect several weeks between submitting an application and receiving a first payment, longer if documentation like a marriage certificate or divorce decree is needed to verify eligibility. That timeline is worth knowing upfront so the process feels like a normal wait, not a sign something has gone wrong.

A woman who suspects she may be eligible for either a divorced spouse benefit or a survivor benefit can request a formal review directly from the Social Security Administration. The eligibility rules covered here are the real ones, and this entitlement exists precisely because a marriage that ended on paper does not always end the financial connection that came from it.

Related reading on rebuilding finances after a major life transition: our guide to finances after divorce covers the broader financial rebuilding process this fits into, including budgeting and credit questions that come up alongside Social Security decisions, and our breakdown of starting an Etsy shop with no money is worth a look if you are also considering a small, independent income stream alongside whatever entitlement you qualify for here. Neither of these benefits, nor a small side income, replaces the other. A woman rebuilding her financial footing after a divorce or a spouse’s death is usually better served by combining several smaller, real sources of stability than by waiting for one single solution to cover everything at once.

People Also Ask

Can I get Social Security from my ex-husband if he remarried?

Yes, his remarriage has no effect on your eligibility for a divorced spouse benefit based on his earnings record, as long as your own marriage to him lasted at least ten years and you are currently unmarried. His current spouse’s benefits are also unaffected by your claim, and the Social Security Administration does not notify him when you file.

Do I lose my ex-husband’s Social Security benefit if I remarry?

If you remarry before age 60, you generally lose eligibility for a survivor benefit based on a deceased ex-husband’s record. Remarrying at age 60 or later does not affect that eligibility, and a divorced spouse benefit from a living ex-husband generally ends upon your own remarriage regardless of age, which is an important difference between the two benefit types.

How much Social Security does a divorced spouse get?

A divorced spouse benefit can be worth up to 50 percent of an ex-husband’s full retirement age benefit if she was married to him for at least ten years, is currently unmarried, and is at least 62 years old. The exact amount depends on his earnings record and the age at which she claims it, with claiming before her own full retirement age resulting in a permanent reduction.

What if my ex-husband never filed for his own Social Security?

You can still claim a divorced spouse benefit on his record as long as you have been divorced for at least two years and he is at least 62 years old, even if he has not yet filed for his own benefits. This two year rule specifically removes the need to wait on his personal timeline, and it is one of the most useful, least publicized parts of the entire system.

Can I collect both my own Social Security and my ex-spouse’s?

No, Social Security does not combine a personal retirement benefit with a divorced spouse or survivor benefit. Instead, it pays whichever single amount is higher between the two, so it is worth requesting an official comparison rather than assuming your own work record automatically produces the larger number. This single fact surprises more women than almost any other detail covered here, and it is worth remembering before making any assumption about which benefit will end up being the right one to claim.