The Hospital Bill Says $4,200. Here Is Exactly What To Do Next.

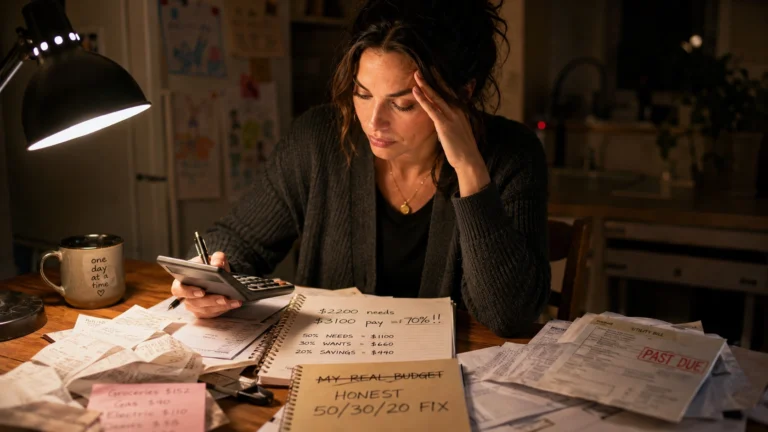

You stand at the counter with the envelope open, and for a second you just look at the number. Not read it. Look at it, the way you’d look at something that doesn’t seem real yet.

For women aged 25 to 50 in the US, especially single moms carrying a household alone, an unexpected hospital bill lands differently than it does for most people talking about “medical debt” in the abstract. It’s not a policy topic. It’s Tuesday, and the number is bigger than what’s in your account.

Here’s what almost nobody tells you in that moment: you have more room to negotiate than the bill implies, and most women never use it. Women report facing medical debt more often than men across nearly every income bracket, and a large share of women who could ask a hospital for financial assistance simply never do. This guide is medical bill help for women who need the actual steps, not the general advice everyone already knows to ignore.

If you can’t pay a hospital bill, don’t ignore it and don’t put it on a credit card first. Nonprofit hospitals, which make up more than half of US community hospitals, are legally required to offer financial assistance to patients who can’t afford care. Call the billing department, ask for their financial assistance or “charity care” policy, and apply before the bill goes to collections. This is real medical bill help women can act on the same day they get the envelope.

Why the Obvious Advice Fails

Everyone says “call the hospital.” Almost nobody tells you what to actually say, or that timing changes your options. Once a bill moves to a collection agency, you lose leverage you had for free the week before.

Here’s the part competitors skip: nonprofit hospitals, which are the majority of hospitals in the US, are required by federal law to offer financial assistance programs as a condition of their tax-exempt status. That’s not charity in the sense of a favor. It’s a legal requirement they’re supposed to publicize clearly, and often don’t.

Generic advice tells you to “negotiate your bill.” It rarely tells you that hospitals are required to screen you for financial assistance before sending your account to collections in many states, or that you can apply for that assistance even after you’ve already been billed. And it almost never tells you that a 2024 analysis found hospitals fail to provide billions of dollars a year in charity care to patients who would have qualified if they’d simply applied.

The Actual Method: Medical Bill Help Women Can Use This Week

This is the order that actually works, not the order most people try out of panic.

Step one: don’t pay it yet, and don’t ignore it either. Both instinctive reactions work against you. Paying immediately with a credit card trades a 0 percent medical bill for 20 percent interest debt. Ignoring it starts the clock toward collections.

Step two: call the billing department and ask one specific question. Ask for their financial assistance policy, sometimes called charity care. Don’t ask “can you lower this,” ask “what is your financial assistance policy and how do I apply.” That phrase gets you routed to the right department instead of a generic payment plan pitch.

Step three: apply, even if you think you won’t qualify. On average, hospitals set eligibility around a household of four earning under roughly $130,000 a year, though this varies significantly by hospital and state, and some hospitals help families who earn more. Many women assume they make too much and never check. Apply first. Let the hospital tell you no.

Step four: ask if you were charged the insured rate. If you have insurance but it didn’t fully cover the visit, or if you were uninsured, ask to be billed at the same rate insured patients pay, not a higher “list price” rate. This single question has saved patients thousands of dollars.

Step five: if you can’t get the bill reduced, negotiate a payment plan you can actually keep. Figure out what you can realistically pay monthly before you call, and offer that number first instead of accepting whatever the hospital proposes.

If the Bill Has Already Gone to Collections

If a collection agency already has your debt, you still have real protections. Federal law gives you rights under the Fair Debt Collection Practices Act: collectors cannot harass you, cannot contact you before 8am or after 9pm, and must stop contacting you entirely if you send a written request. If you’re sued over medical debt, free legal aid is available in most areas, and people over 60 or below certain income thresholds typically qualify automatically.

The Hard Numbers: What Medical Debt Actually Looks Like for Women

The exact scale of medical debt in the US varies depending on how it’s measured, credit reports capture some of it, household surveys capture more, but a few figures are consistently documented and worth knowing.

| Fact | Source |

|---|---|

| Nonprofit hospitals, over half of all community hospitals, must offer financial assistance to keep their tax-exempt status | Consumer Financial Protection Bureau |

| A 2024 analysis found hospitals fail to provide at least $14 billion a year in charity care to patients who would have qualified | AARP reporting on Dollar For analysis |

| Households with medical debt report cutting spending on food and household basics, and spending down savings to cover bills | Peterson-KFF Health System Tracker |

| A first-time mother’s childbirth bill going to collections was linked to a lower likelihood of having a second child within two years | Penn State study, reported via Spotlight PA |

That last one is worth sitting with. Medical debt doesn’t just strain a budget. It quietly changes decisions that have nothing to do with money on paper.

What Changes After You Do This

The bill doesn’t disappear the moment you call. But something shifts almost immediately: you go from being a passive target of collections to an active applicant with a paper trail. That paper trail matters more than it sounds like it should.

Within a few weeks of applying for financial assistance, most hospitals give you a written determination. Even a partial reduction changes the math entirely, and a payment plan you actually chose, rather than one imposed after a missed deadline, is far easier to keep.

The bigger shift is quieter. You stop opening mail with dread, because you already know what’s coming and you already have a plan for it.

Where to Start This Week

The single most useful thing you can do today is call the hospital’s billing department and ask for their financial assistance policy by name. Not a payment plan. The financial assistance policy specifically, since that’s the one most patients never ask about directly.

If your bill has already gone to collections, know your rights under the Fair Debt Collection Practices Act before that next call comes in, and reach out to a local legal aid office if you’re facing a lawsuit over the debt. If you’re also working on stabilizing your overall budget while you handle this, my guide on building your emergency fund walks through how to create that first buffer so the next unexpected bill doesn’t hit as hard.

Medical bill help for women isn’t complicated. It’s mostly about asking the right question before the wrong deadline passes.

People Also Ask

Can hospitals really forgive medical debt?

Yes. Nonprofit hospitals, over half of US community hospitals, are required by federal law to offer financial assistance programs to patients who can’t afford care, and many for-profit hospitals offer similar programs voluntarily. You can apply before treatment, at the time of billing, or even after your account has gone to collections. This is genuine medical bill help women often don’t realize is available.

What happens if I just don’t pay a hospital bill?

Unpaid medical bills can eventually be sent to a collection agency, which may affect your credit report and could lead to a lawsuit in some cases. However, you have protections under the Fair Debt Collection Practices Act, and applying for financial assistance, even late, is almost always better than ignoring the bill entirely.

Should I put a hospital bill on a credit card?

Generally no, at least not as a first step. Medical debt on a bill typically doesn’t carry interest, while credit card balances often carry 20 percent or higher interest. Explore financial assistance and payment plans directly with the hospital first, since paying with a card can turn a manageable bill into a much larger, interest-bearing debt.

Do single moms qualify for hospital financial assistance more easily?

Eligibility depends on household income and size, not marital status specifically, but because financial assistance thresholds are based on household income relative to family size, single-income households often qualify at a lower income level than a two-income household would. It’s worth applying regardless of your assumptions about whether you’ll qualify.