Single Mom Budget: The Honest 50/30/20 Fix

A single mom budget built on the standard 50/30/20 rule often breaks before it even gets started, and almost nobody says that part out loud. I sat down one Sunday night with a calculator and my pay stub, ready to follow the percentages everyone recommends, and the fifty percent needs category was already gone before I had even added groceries, gas, or a single utility bill.

I closed the laptop and sat there for a minute feeling like I had failed at math I had not even finished doing. Except the problem was never my math. The percentages themselves were built around an assumption that does not hold for a lot of single income households, especially once childcare enters the picture.

The Reality Check

The original 50/30/20 rule splits take home pay into fifty percent needs, thirty percent wants, and twenty percent savings or debt. For a two income household with no childcare costs, that split can genuinely work. For a single mom budget, it almost never starts that way.

Childcare alone often runs close to twenty percent of household income on its own, before rent, before groceries, before anything else gets considered. Add rent or a mortgage on top of that, and needs frequently land somewhere between sixty and seventy percent of take home pay, not fifty. When the framework assumes fifty and reality delivers seventy, the gap does not mean you are bad with money. It means the framework was calibrated for a different household than yours.

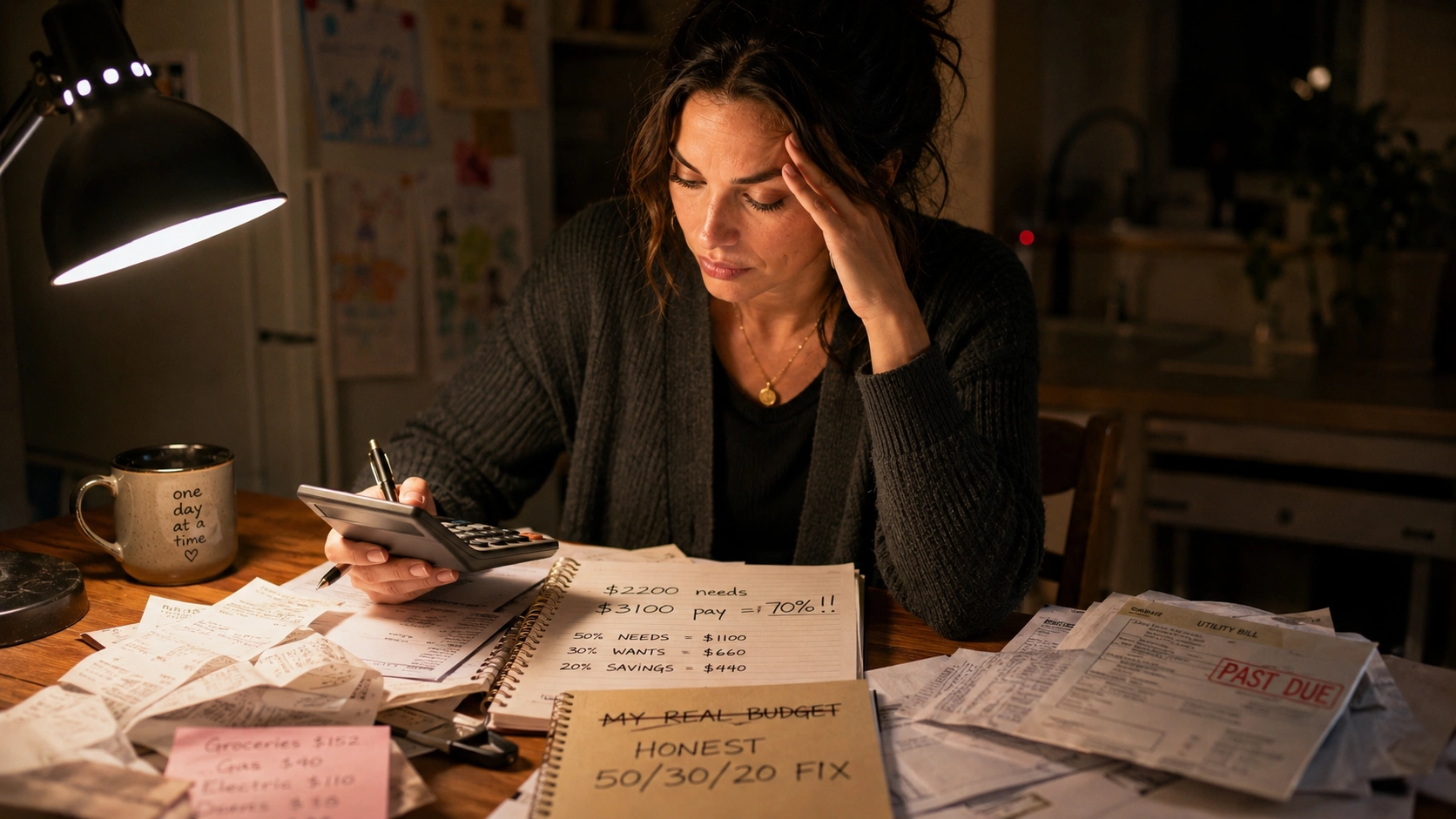

Once I actually sat down and listed every expense for one full month, the picture became clear in a way vague worry never had. Rent. Daycare. Groceries. Gas. Utilities. Insurance. Minimum debt payments. Adding those up and dividing by my take home pay gave me a real percentage, not the one a generic article had told me to expect.

The Shift

The shift that changed everything was adjusting the percentages themselves rather than trying to force my spending to match numbers that were never going to fit. A single mom budget built on sixty percent needs, twenty percent wants, and twenty percent savings and debt is not a smaller or lesser version of 50/30/20. It is the same framework, recalibrated for a household where childcare and housing genuinely take up more room.

For some months, needs honestly run closer to seventy percent, and wants shrink to fifteen. That is not failure either. It is information, and information is something you can work with in a way that guilt never lets you.

The other shift was realizing that when fixed expenses are locked in and money still feels tight, the place to look is not the needs category at all. It is the wants category, where small recurring costs hide more easily than they do in a rent payment.

How a Single Mom Budget Actually Holds Together

Here is what this looked like with real numbers, using a take home pay of three thousand dollars a month.

At sixty percent, needs get one thousand eight hundred dollars. That covered rent at eleven hundred, daycare at four hundred, groceries at two hundred, and utilities and gas combined at one hundred. Wants at twenty percent, six hundred dollars, covered everything from my daughter’s after school activities to the occasional dinner out. Savings and debt at the remaining twenty percent, six hundred dollars, went toward a small emergency fund and extra payments on one credit card.

The first month, the wants category was where I found the most room. A streaming subscription I had forgotten about. A clothing swap group at my daughter’s school that meant I stopped buying things she would outgrow in eight weeks anyway. Together those two things freed up about a hundred and twenty dollars a month, money that moved straight into the savings category without changing my actual lifestyle in any way I noticed day to day.

Where Meal Prepping Fits Into the Numbers

The two hundred dollar grocery number above came down from closer to three hundred once I started planning a week of dinners around what was already in the freezer and shopping with an actual list. Theme nights helped too, taco night and pasta night meant fewer decisions and less food going bad before we got to it. That hundred dollar difference each month was the single biggest shift inside the needs category itself.

The Hard Numbers

The habit that made the rest of this sustainable was automating savings the same day my paycheck arrives, before I see the number sitting in checking. Twenty five dollars a week, moved automatically into a separate account, comes out to thirteen hundred dollars a year without a single manual decision.

According to the Consumer Financial Protection Bureau, automating savings transfers immediately after pay arrives is one of the most effective ways to build savings specifically because it removes the moment of choice, which research consistently shows is where most saving plans quietly fail. For a single mom budget, removing that one decision point matters more than the dollar amount itself, because decision making is the resource there is the least of by the end of most days.

On top of automation, a single ten minute check each Sunday, looking at the week ahead for any school fees, due dates, or events that need cash, catches the small surprises before they become emergencies. Ten minutes a week is just under nine hours a year, spent in exchange for far fewer moments of being caught off guard.

Honest Life After This

Thirteen hundred dollars a year in automated savings and a hundred dollars a month from meal planning did not transform everything overnight, and I want to be honest about that. What changed was smaller and showed up faster than the dollar amounts suggest.

I stopped dreading the start of the month, because I finally knew my real percentages instead of the ones a generic article had assumed for me. That clarity paired well with something I wrote about before, when I worked through a way to split larger bills across paychecks so they stop landing as one overwhelming hit, which fit naturally once the Four Walls were already accounted for first.

The Sunday ten minute check became the thing that held it all together, not because it solved anything dramatic, but because it meant nothing ever caught me by surprise two days before it was due.

Straight Talk Closing

If 50/30/20 has never worked for you, that was never a reflection of your discipline or your math. The percentages were built around a household that is not yours, and adjusting them is not cheating the system.

Write down your real numbers this week, your actual needs as a percentage of take home pay, not the percentage a generic rule assumes. A single mom budget that starts with your real numbers, protects food, shelter, transportation, and utilities first, and automates even twenty five dollars a week is not a smaller plan. It is the right one.

Read More:

Newborn Income Ideas: 7 Simple Ways to Earn $2,500

Spending Leak: The Honest 57% Habit